Weekly Recap

Stocks enjoyed a melt-up during a quiet macro period ahead of this week’s May CPI report and the June FOMC meeting. Cyclicals generally outperformed despite fairly tepid (and limited) macro data, suggesting that duration played a key role in relative sector performance. Small caps were also better, driven in large part by their higher cyclical exposure.

Rates backed up a bit last week as market participants continued to price in a “higher for longer” Fed policy path, pushing high grade bond prices lower. Spreads have stabilized after widening into the debt ceiling deadline and then rallying when a deal was struck and a US default was avoided.

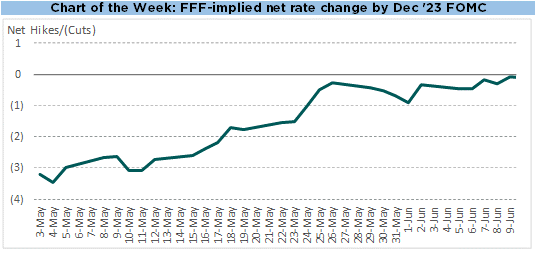

Fed fund futures were little changed on the front end last week, still pricing in a 30% chance of a hike at the June meeting. But odds of one or more rate cuts by year-end continue to ease lower, and have fallen significantly since the first few days after the May FOMC meeting. At the close on May 3rd (after the FOMC rate announcement and press conference), futures markets were pricing in no more hikes and 3.5 rate cuts by year-end.

Fast forward to the present, and futures markets imply that there is likely to be a hike at one of the next two meetings, and one cut by year-end, for a net rate change of zero. See the Chart of the Week for a time series of year-end net Fed Funds rate changes from May 3rd through Friday’s close.

Albion’s “Four Pillars”

Economy & Earnings

The US economy enjoyed a strong second half of 2022, but growth has slowed in early 2023 and corporate operating margins have fallen as labor and input cost pressures bite. Albion’s base case expectation is that the US economy will enter recession in 2023, putting downside pressure on earnings.

Valuation

The S&P 500’s forward P/E of 18x is above the long run average, so valuation could be a mild headwind to future returns. More predictive metrics like CAPE, Tobin’s Q, and the Buffett Indicator (Mkt Cap / GDP) suggest that compound annual returns over the next decade are likely to be in the mid single digits.

Interest Rates

Rates rose dramatically in 2022 in response to a sharp pivot in monetary policy, and have remained elevated in 2023 as progress on inflation has been slower than hoped. Futures markets are currently pricing one additional 25bp rate hike over the summer, and one rate cut near the end of the year.

Inflation

After reaching 40yr highs in spring of 2022, inflation has moderated somewhat over the past 12 months. Goods inflation has fallen due to softening demand and excess inventory, while services inflation remains elevated, in part due to shelter costs which are somewhat lagged.