Executive Summary

Creating a reliable income stream in retirement takes more than just saving—it requires strategy. In this post, we’ll walk through five smart ways to get the most out of what you’ve built:

- Get the most from Social Security. When you file matters. Understanding your options—including spousal and survivor benefits—can add up to hundreds of thousands of dollars over time.

- Withdraw your money tax-efficiently. Where you pull income from each year can impact how much you keep. Coordinating withdrawals across taxable, tax-deferred, and tax-free accounts can stretch your savings and lower your tax bill.

- Do an annual tax check-up. Your income and the tax rules change every year. Reviewing your situation regularly opens up opportunities—like Roth conversions or tax-smart charitable giving—that can save you money long-term.

- Watch for policy updates. Shifts in tax law, Medicare premiums, or Social Security rules can affect your plan. Stay informed so you can adjust before small changes become costly surprises.

- Keep your plan flexible. Life doesn’t follow a spreadsheet. Revisiting your retirement strategy regularly ensures it still fits your goals, your lifestyle, and whatever life throws your way.

In many ways, approaching retirement is like climbing a new mountain. The view at the top is worth the climb—but the journey has its own steep terrain, loose footing, and changing weather to navigate along the way.

Retirement is no different.

On the one hand, it marks the beginning of a new and exciting chapter, powered by the ability to do what you want, when you want, with the people you want, for as long as you want (which as best selling personal finance author Morgan Housel says: “Is the best dividend that exists in finance.”) But, on the other hand, it also brings unique challenges and unknowns.

And one of those unknowns is the reality that once you retire, you can no longer rely on your job for a paycheck. Instead, you must create that retirement paycheck on your own, often drawing on multiple accounts (each with unique tax considerations) and income sources (some guaranteed, and some not) to fund your life.

If you’re within five years of retiring, it’s also worth reviewing the three critical steps to prepare for retirement to make sure you’re laying the right groundwork—financially, emotionally, and logistically.

In this article, we’ll explore five smart strategies to maximize your retirement income and help you reduce uncertainty as you head into your golden years.

Strategy #1: Squeeze All The Juice Out Of Social Security

When it comes to retirement income, Social Security is one of the most important decisions you’ll make. And like most things in financial planning, there’s no one-size-fits-all answer—the right filing strategy depends on your overall financial picture, your health, and your goals.

Start by understanding your Full Retirement Age (FRA)—the age at which you’re entitled to your full benefit. For most people retiring today, FRA falls between 66 and 67, depending on your birth year. If you file early (as soon as age 62), your benefit will be permanently reduced—up to 30% lower if you start right at 62. If you delay filing past FRA, your benefit increases by about 8% for each year you wait, maxing out at age 70. Over time, the difference between claiming early and waiting can add up to hundreds of thousands of dollars, especially if you live a long life.

Timing is even more critical if you’re married.

Spousal benefits allow a lower-earning spouse to receive up to 50% of the higher earner’s benefit. To claim spousal benefits, the higher-earning spouse must file first, and filing before FRA reduces the spousal benefit as well. In addition, when one spouse passes away, the surviving spouse keeps the higher of the two benefits. That means if the higher earner delays filing, it can increase the surviving spouse’s income for life—a critical consideration for couples where one partner is expected to outlive the other.

It’s also helpful to understand your breakeven age—the point at which the total value of delaying benefits surpasses what you would have received by claiming early. For many retirees, the breakeven point falls between age 77 and 83, depending on your benefit amount and filing strategy. If you’re healthy and expect to live well into your 80s or beyond, delaying could be the better move. But if you have health concerns or need income sooner, filing earlier may be the more practical choice.

Ultimately, Social Security is just one piece of your retirement paycheck—but it’s a foundational one. It offers inflation-adjusted, guaranteed income for life, and in many cases, it can act as a buffer that helps protect you during market downturns. The key is to evaluate the tradeoffs, understand how the rules apply to your situation, and make a decision that fits into the broader context of your financial plan. If you’re not sure which path makes the most sense, working with a financial advisor can help you “squeeze all the juice” out of this critical benefit.

Strategy #2. Implement a Tax-Efficient Withdrawal Strategy

One of the most overlooked ways to maximize your retirement income is by carefully managing where your withdrawals come from each year. Most retirees have a mix of account types—traditional IRAs and 401(k)s (tax-deferred), Roth IRAs (tax-free), and brokerage accounts (taxable). Each of these is taxed differently, and the order in which you draw from them can have a big impact on your lifetime tax bill. For instance, early in retirement, you might lean more on taxable accounts and strategically convert IRA dollars to Roth while your income is relatively low.

Later on, Roth accounts can also provide tax-free income in years when your taxable income is already high, helping you stay below key income threshholds.

For example, imagine a retiree who needs to withdraw an extra $15,000 to cover a large one-time expense. If they take the money from their IRA, it increases their taxable income—not only pushing more of their Social Security into the taxable range but also reducing or eliminating subsidies they’re receiving through the Affordable Care Act (ACA). In some cases, that $15,000 withdrawal could result in thousands of dollars in additional taxes and lost benefits. But if that same amount is withdrawn from a taxable brokerage account or Roth IRA, where only a portion is subject to capital gains tax or completely tax-free, the impact might be far less severe. Coordinating withdrawals with your broader tax and healthcare situation can make a significant difference in how long your portfolio lasts.

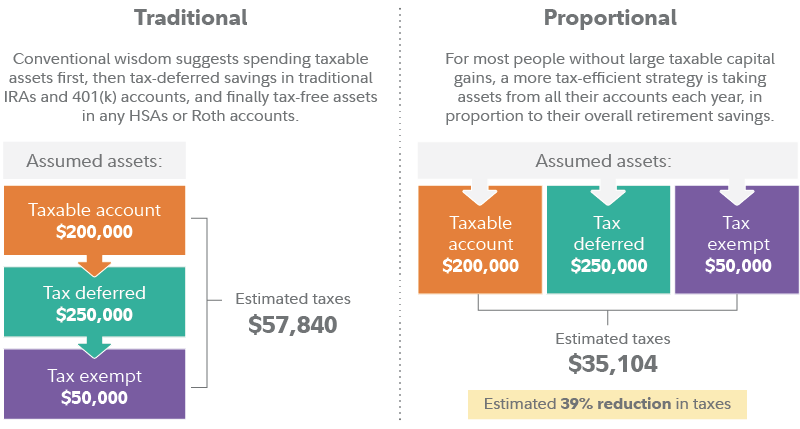

It’s a common belief that retirees should draw from taxable accounts first, then tax-deferred, and finally tax-free. But as the example below from Fidelity shows, a more balanced approach—pulling proportionally from each type—can lead to dramatically lower taxes over time.

How Withdrawal Order Affects Your Lifetime Tax Bill

It’s also important to plan around Required Minimum Distributions (RMDs), which begin at age 73 for most retirees (and 75 for those born in 1960 or later). If your traditional retirement accounts are large, those RMDs can create an income spike that pushes you into a higher bracket. Planning ahead by “filling up” lower brackets with partial Roth conversions in your 60s—or withdrawing pre-RMD strategically—can help smooth your tax picture over time. A withdrawal plan isn’t static; it needs to evolve with tax laws and your spending needs.

Strategy #3. Review Your Tax Situation Each Year

Taxes don’t disappear in retirement—they just change form.

Each year, retirees make decisions that can either add up to thousands in unnecessary taxes or lead to years of meaningful tax savings. A yearly review can help you evaluate whether it makes sense to realize capital gains in a low-income year, offset gains with tax-loss harvesting, or accelerate deductions through charitable giving. Retirement often opens up new opportunities for tax savings, especially if you’re no longer earning wages. You may now qualify for deductions like high medical expenses or be able to take advantage of tax-efficient giving strategies such as Qualified Charitable Distributions (QCDs) once you reach age 70½.

One powerful strategy to evaluate each year is Roth conversions. These can be especially impactful in the early years of retirement—after you’ve stopped working but before RMDs and Social Security kick in. By intentionally converting portions of a traditional IRA to a Roth while your taxable income is low, you can pay tax at a lower rate now and reduce the size of future RMDs. Doing this over multiple years can create a more balanced tax picture and lower your lifetime tax bill.

The key is that these decisions require foresight—once the year ends, many tax planning opportunities disappear.

Strategy #4. Stay On Top Of New Changes

Retirement planning doesn’t end when you stop working—it evolves constantly.

Tax laws, Social Security rules, RMD ages, and Medicare premiums are all subject to change, and even small tweaks can have a ripple effect on your income. For example, recent legislation (like the SECURE Act and its sequel) has already changed RMD ages and beneficiary rules for inherited IRAs. COLA adjustments to Social Security can bump up income, which in turn might affect your tax bracket or Medicare premiums.

Staying informed helps you make timely decisions and avoid unintended tax consequences.

Medicare premiums, in particular, are often misunderstood. They’re income-based, so if your Modified Adjusted Gross Income (MAGI) crosses certain thresholds—even by a dollar—you could end up paying hundreds more per month in IRMAA surcharges. That’s where smart tax planning and withdrawal coordination comes in. In some years, it will be essential to know where you are drawing income from and how it will affect your tax picture.

Keeping up with these rule changes doesn’t mean you have to become an expert—but it does mean revisiting your plan each year and adapting as needed.

Strategy #5. Review and Adjust Your Plan Along The Way

Your financial plan is a living document, not a one-and-done checklist.

Retirement is full of curveballs—markets shift, health events arise, family needs change, and your personal goals may evolve too. That’s why it’s so important to revisit your plan annually to make sure it still fits your life. Even small changes, like a new travel goal or deciding to downsize your home, can impact your income needs, investment allocation, and withdrawal strategy. And on the flip side, major unexpected events—like supporting an adult child or dealing with long-term care—can require deeper recalibration.

Annual financial check-ups are a great time to review your current cash flow, make sure your spending plan still aligns with your values, assess your emergency reserves, and rebalance your portfolio if needed. It’s also a good time to run “what if” scenarios—What if the market dips next year? What if you live to age 100? What if you want to give more during life? These reviews don’t just provide peace of mind—they help you stay proactive instead of reactive. Flexibility is one of the most valuable assets in retirement. The more willing you are to course-correct along the way, the more resilient—and fulfilling—your retirement will be.

Retirement isn’t just about income strategies—it’s about enjoying the life you’ve worked hard to build. For ideas on how to live your golden years with purpose and intention, check out our post on How to Make the Most of Your Golden Years.

In the end, retirement can be an exciting and rewarding phase of life, but it requires careful planning and ongoing adjustments to maximize your income and reduce uncertainty. By implementing these five strategies—maximizing Social Security, drawing income tax-efficiently, reviewing your taxes annually, staying informed about key changes, and staying flexible—you can reduce uncertainty and build a more confident retirement.

Albion Financial Group is an SEC registered investment advisor. The information provided is intended solely for educational purposes and should not be construed as an offer or solicitation for the purchase or sale of any particular securities product, service, or investment strategy. Past performance is not indicative of future performance. Additional information about Albion Financial Group is also available on the SEC’s website at www.adviserinfo.sec.gov under CRD number 105957. Albion Financial Group only transacts business in states where it is properly registered, notice filed or excluded or exempted from registration or notice filing requirements.

{kind=link}