Weekly Recap

Last week’s headline event was undoubtedly the FOMC meeting, and for the first time in 15 months the Fed kept overnight interest rates unchanged. While this outcome was widely anticipated, investors were keen to hear from Jerome Powell as to the likely forward path of monetary policy. His commentary was decidedly hawkish, as was the updated Summary of Economic Projections which showed that multiple additional rate hikes are still possible. Powell was also quite firm in his pronouncement that no rate cuts would be forthcoming later this year.

The Fed’s “hawkish pause” did little to dent the market’s enthusiasm, however, as stocks rose yet again. The S&P 500 finished higher for the 5th week in a row, and has officially entered bull market territory after rising more than 23% from the October 2022 lows. Relatively benign inflation data may have helped. Headline CPI fell to 4.0% y/y while core CPI dropped 20bp to 5.3% y/y, and PPI (final demand) fell to just 1.1% y/y. Meanwhile, the University of Michigan’s gauge of 1y forward inflation expectations fell 90bp to 3.3%, a clear sign that consumers are starting to view inflation as less of a near term risk.

Bond markets reacted to Fed day with a twist, as short yields rose while longer yields fell. Fed Funds Futures markets are pricing better than even odds of a rate hike at the July meeting (Jerome Powell inadvertently said “skip” to describe the June meeting, and then quickly corrected himself), and for the first time futures are now pricing in no rate cuts before year-end. In the game of “rate cut chicken” between the Fed and futures markets, it appears that the Fed has finally won.

Albion’s “Four Pillars”

Economy & Earnings

The US economy enjoyed a strong second half of 2022, but growth has slowed in early 2023 and corporate operating margins have fallen as labor and input cost pressures bite. Albion’s base case expectation is that the US economy will enter recession in 2023, putting downside pressure on earnings.

Valuation

The S&P 500’s forward P/E of 18x is above the long run average, so valuation could be a mild headwind to future returns. More predictive metrics like CAPE, Tobin’s Q, and the Buffett Indicator (Mkt Cap / GDP) suggest that compound annual returns over the next decade are likely to be in the mid single digits.

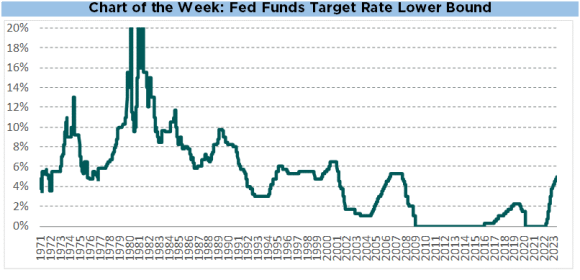

Interest Rates

Rates rose dramatically in 2022 in response to a sharp pivot in monetary policy, and have remained elevated in 2023 as progress on inflation has been slower than hoped. Futures markets are currently pricing one additional 25bp rate hike over the summer, with no rate cuts expected before year-end.

Inflation

After reaching 40yr highs in spring of 2022, inflation has moderated somewhat over the past 12 months. Goods inflation has fallen due to softening demand and excess inventory, while services inflation remains elevated, in part due to shelter costs which are somewhat lagged.